1-Year Review of Prediction Performance

We aim to publish a review of prediction performance every 6 months, as a checkup on the virtue of tsterm engine. Since launch last March, if we use the net prediction out of the ensemble voting for synthetic trading position, the findings are consistent with the last review so far:

For assets that demonstrated clearest long-term trend, the active trading strategy can hardly beat the passive one, but always cuts the maximum drawdown to about half;

For other assets, the predictions have an edge.

More specifically, we shall see for our setting, over the last year,

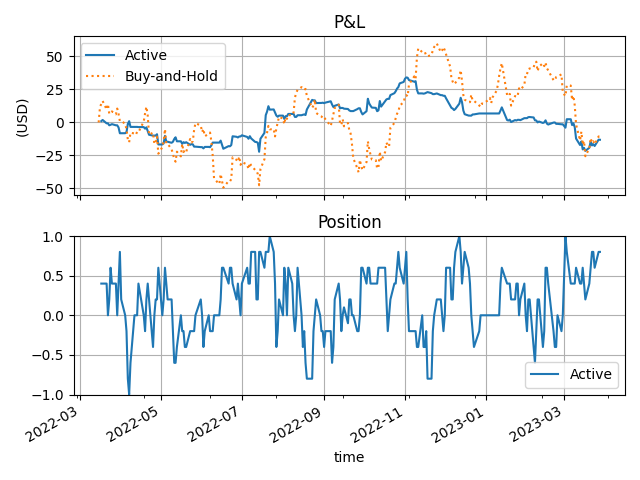

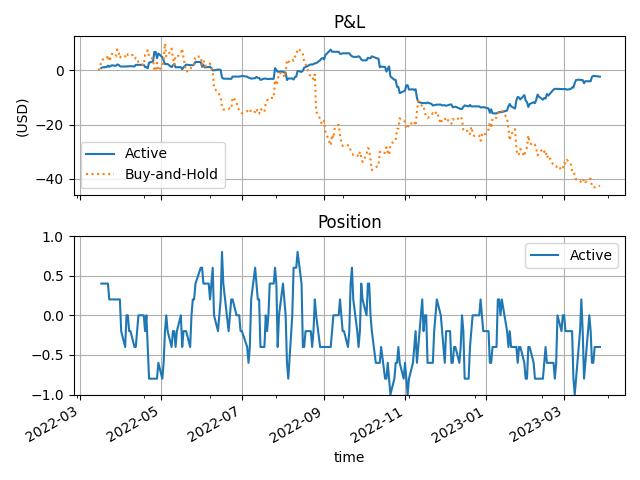

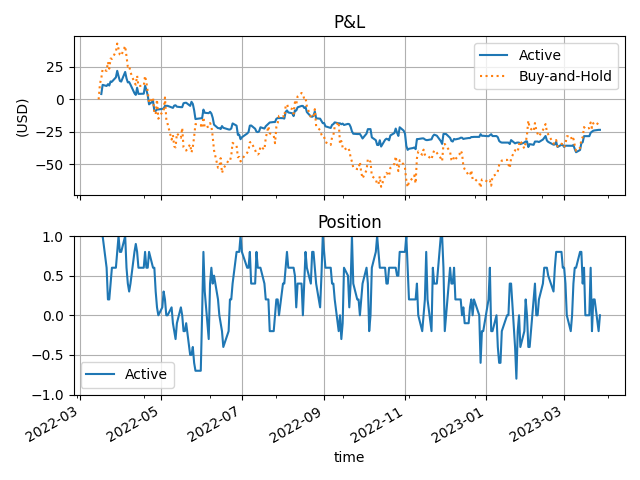

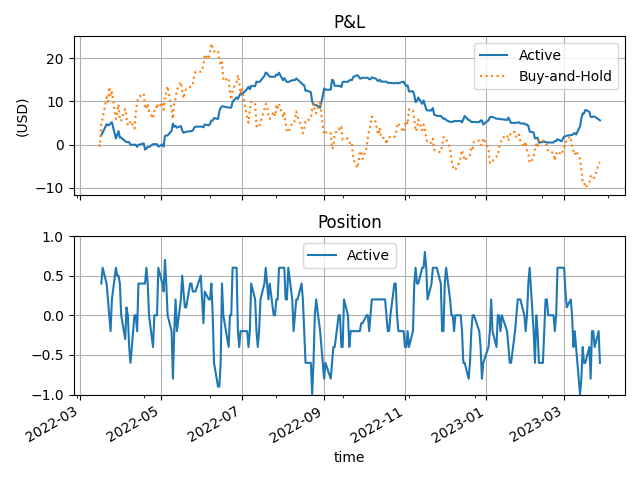

Most prominent US stocks were unbeatable, with some exceptions as Microsoft MSFT (tech), or 3M MMM (industrial).

US Nasdaq 100, S&P 500 indices were unbeatable;

Gold was unbeatable;

Bitcoin was unbeatable.

When we say “unbeatable”, it means the synthetic dynamic trading couldn’t beat the static buy-and-hold strategy.

Before we proceed, first the disclaimer that tsterm provides a causal analytics service “as it”. We do not offer advisory for management of money.

Setting

2-day ahead forecast horizon

ensemble majority voting. So if on one day, 70% of child models predict up, 20% of child models predict down, and 10% are “undecided”, there would be a net majority of 50% that predict up. The synthetic trading position would be correspondingly long 0.50 shares.

zero trading cost

no leverage

the buy-and-hold strategy always holds 1 share

Results

We go by asset classes. First single stocks,

Apple Inc. AAPL

Microsoft MSFT

Goldman Sachs GS

3M MMM

Then US equity indices.

US Nasdaq 100 ETF QQQ

US S&P 500 Index ETF SPY

US DJIA ETF DIA

Next up the currencies.

EURUSD

GBPUSD

Gold ETF GLD

The commodities.

US WTI Crude Oil ETF USO

Brent Crude Oil ETF BNO

We don’t suggest using tsterm for instruments of high volatility. For the purpose of information, we gave results on cryptocurrencies.

BTCUSDT

ETHUSDT

We’d appreciate any thoughts or feedback. Thanks a lot.