2025-03: semiconductor resetting to 2023-2024 level, some consumer service resetting to 2020 level driving US equity 6 months out

NVDA, SNPS resetting to 2023-2024 level, UPS resetting to 2020 level driving US equity 6 months out.

If one searches for “QQQ.US;SPY.US;DIA.US” (without the quotation marks) on tsterm.com, one will find the top causally predictive factors for (the probability distribution of) their prices on the day in six months are

Nvidia NVDA (semiconductor)

United Parcel Service UPS (courrier service)

Synopsys SNPS (semiconductor design)

Duke Energy DUK (oil and gas energy)

NVDA

How NVDA could have been chosen as causal predictor for the three US stock indices six months out? NVDA became more volatile since mid-2024. The three US stock indices became more volatile since February 2025. The lead time was about 6 months (the forecast horizon).

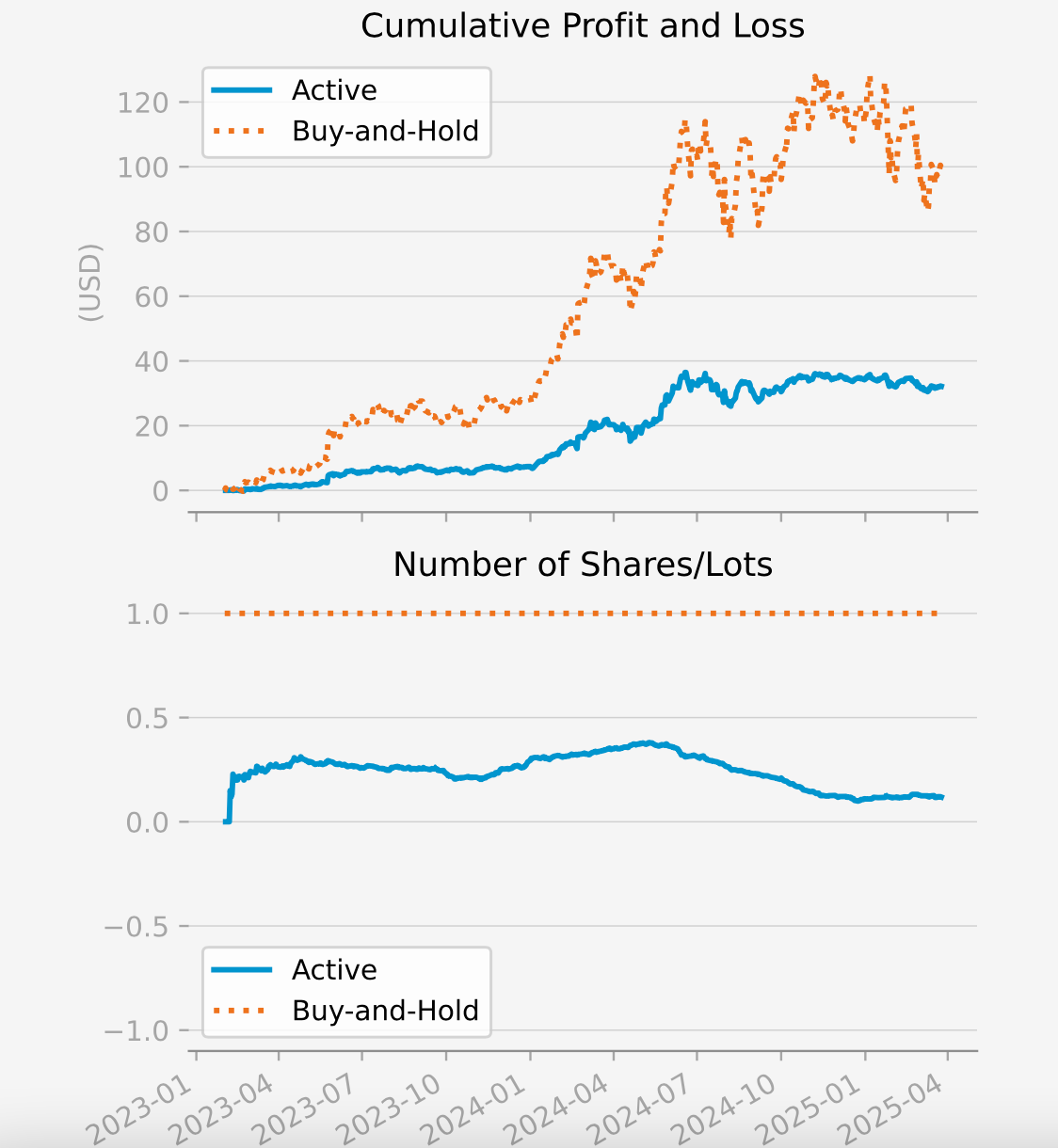

Moreover, if one searches for NVDA on tsterm.com, one may see the daily position (in chart “Number of Shares/Lots”) for NVDA itself is getting ever lower since mid-2024. The Sharpe ratio (that measures the trade-off between risk and return) of the active strategy (trading NVDA) 1.33 is higher than that of the passive buy-and-hold 0.96, so the active strategy was better in this aspect. One just has to multiple the positions by a constant to achieve a higher return at the end, but this characteristic of risk-return does not change in doing so.

The next-day position is the average of signal computed daily over the most recent 6 months (the forecast horizon). The “signal” is the majority vote of “up”s and “down”s everyday.

Support tsterm.com

Would you like predictions for BTCUSD, TSLA.US, etc., and intra-day update for more real-time experience? Support tsterm.com with $5 a month.